Is Your Home Insured Against Natural Disasters?

Hurricanes Helene and Milton caused flooding and mudslides on a scale some commentators deemed as only once in a thousand year events. The destruction they caused cost some people their lives and many more their homes. The unfortunate reality is that many, if not most, insurance policies do not cover key natural disasters including flooding, mudslides and earthquakes. The damage from these storms, combined with the lack of insurance coverage from them, can mean financial ruin for the those who are unfortunate enough to experience them.

According to the Congressional Budget Office (CBO), 30% of losses attributable to natural disasters in 2023 were not covered by insurance.

However, it is possible to protect yourself against the financial ruin caused by natural disasters. Perhaps the best place to start is with an understanding of what your potential risks are.

Climate Change and Natural Disasters On the Rise

As with most topics, the more you know the better prepared you will be. When it comes to natural disasters like hurricanes, wildfires, floods, mudslides and earthquakes we have some compelling data that suggests we can expect the frequency and severity of these events to increase on average. Let's take a look at what the National Oceanic and Atmospheric Agency (NOAA) has to say about the matter.

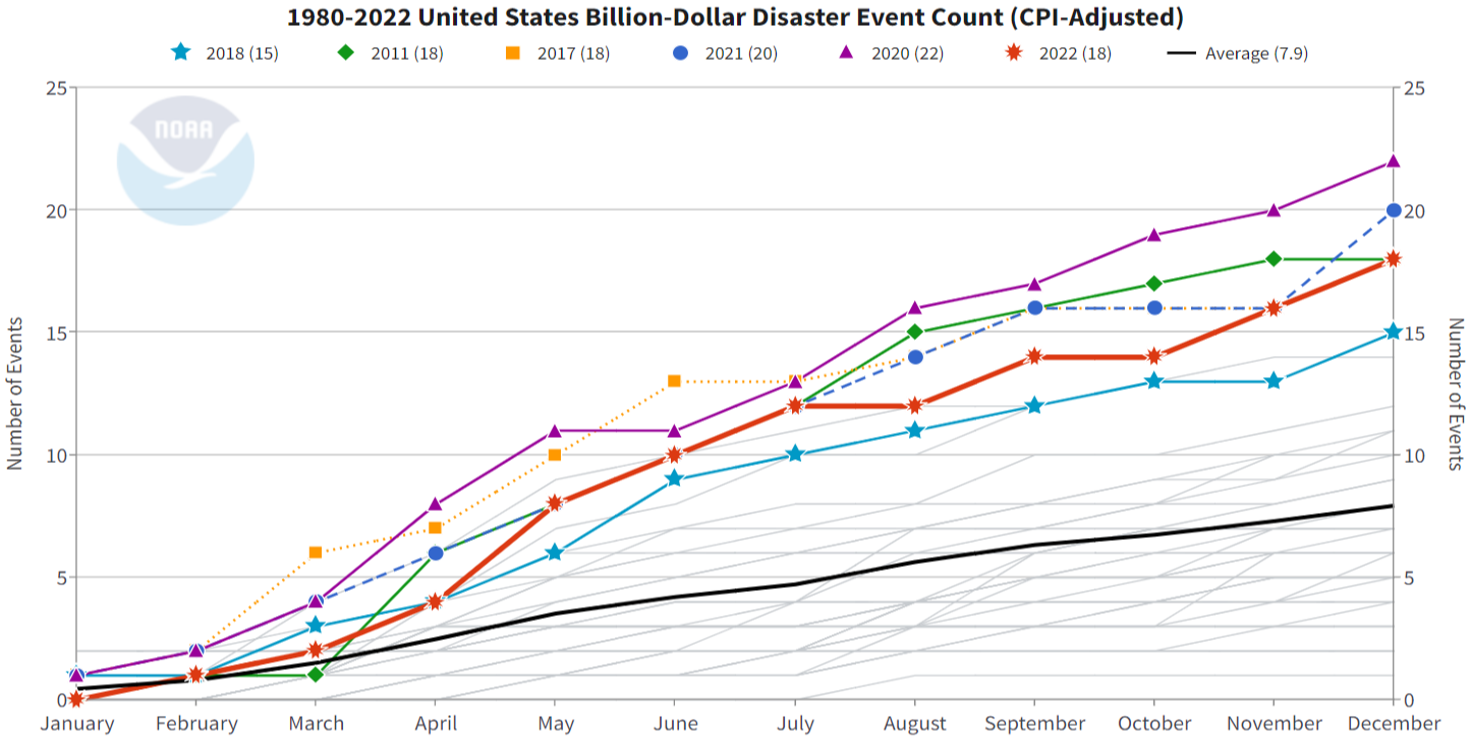

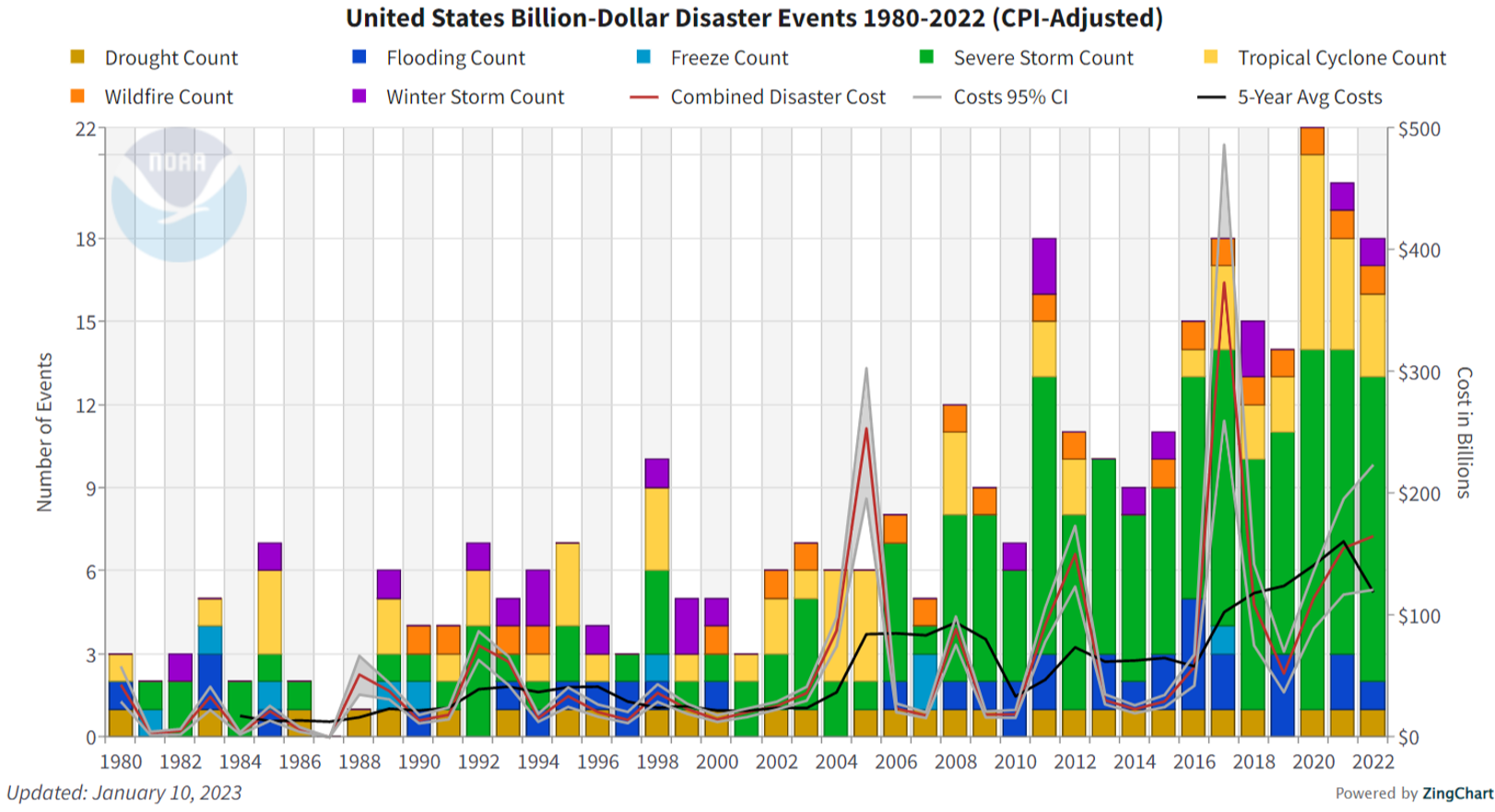

NOAA's data indicates a clear trend upwards in the number of "Billion-Dollar Disasters" over the most recent 42 year period. This data suggests that the costs of natural disasters are increasing.

Another way to visualize the data follows. I'll draw your attention to the line graph that is overlayed below and point out that the costs are adjusted for inflation. In other words, we are trending higher in both the number of sever events ad their costs after controlling for inflation.

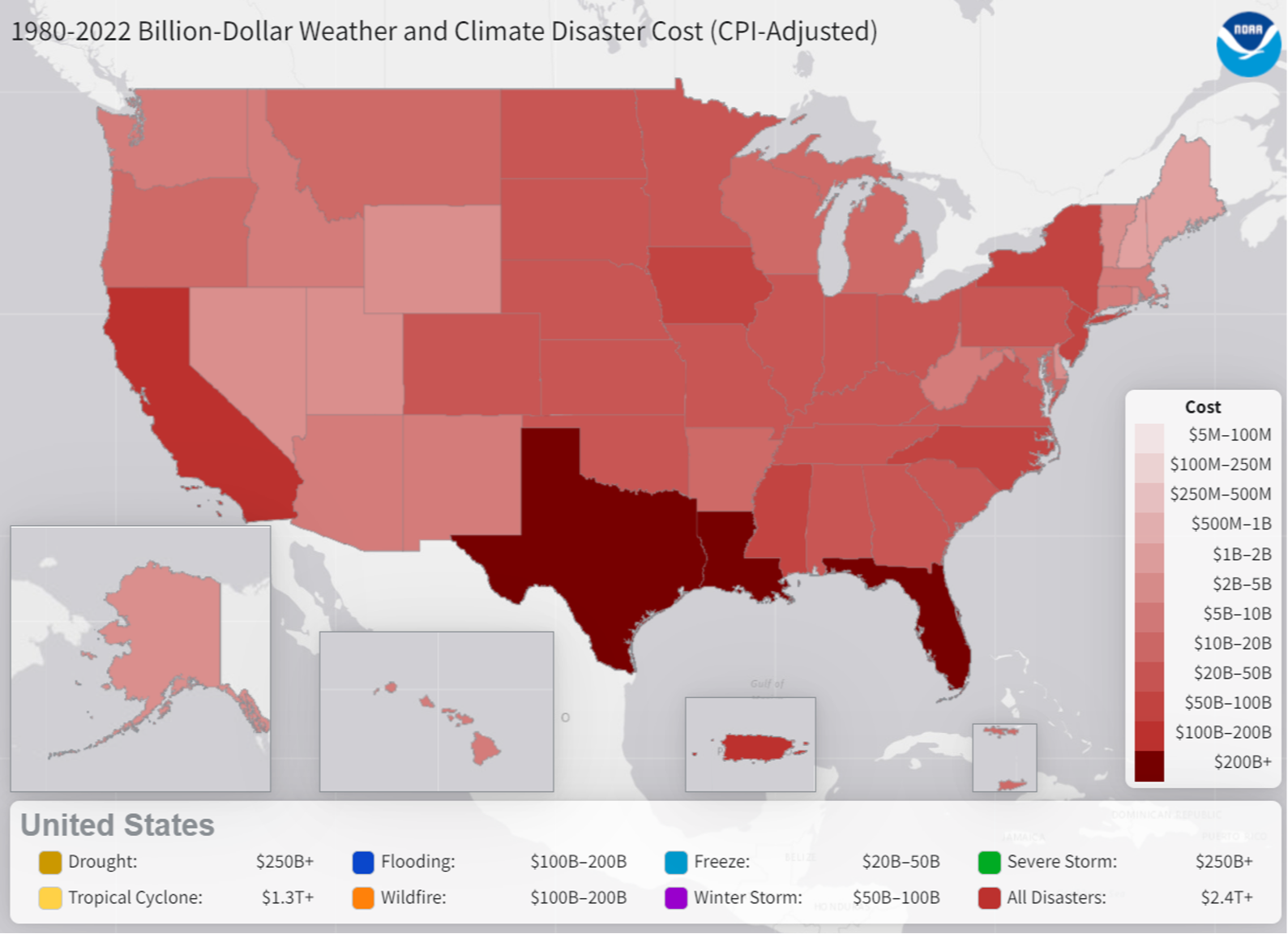

Of particular importance to us, as Financial Commandos, is information that is actionable and allows us to make better financial decisions. Afterall what good is this information if you can't do anything with it? As every good commando knows, terrain matters. Here we see this in action because different geographies are exposed to different types of natural disasters, and at varying levels of regularity and severity.

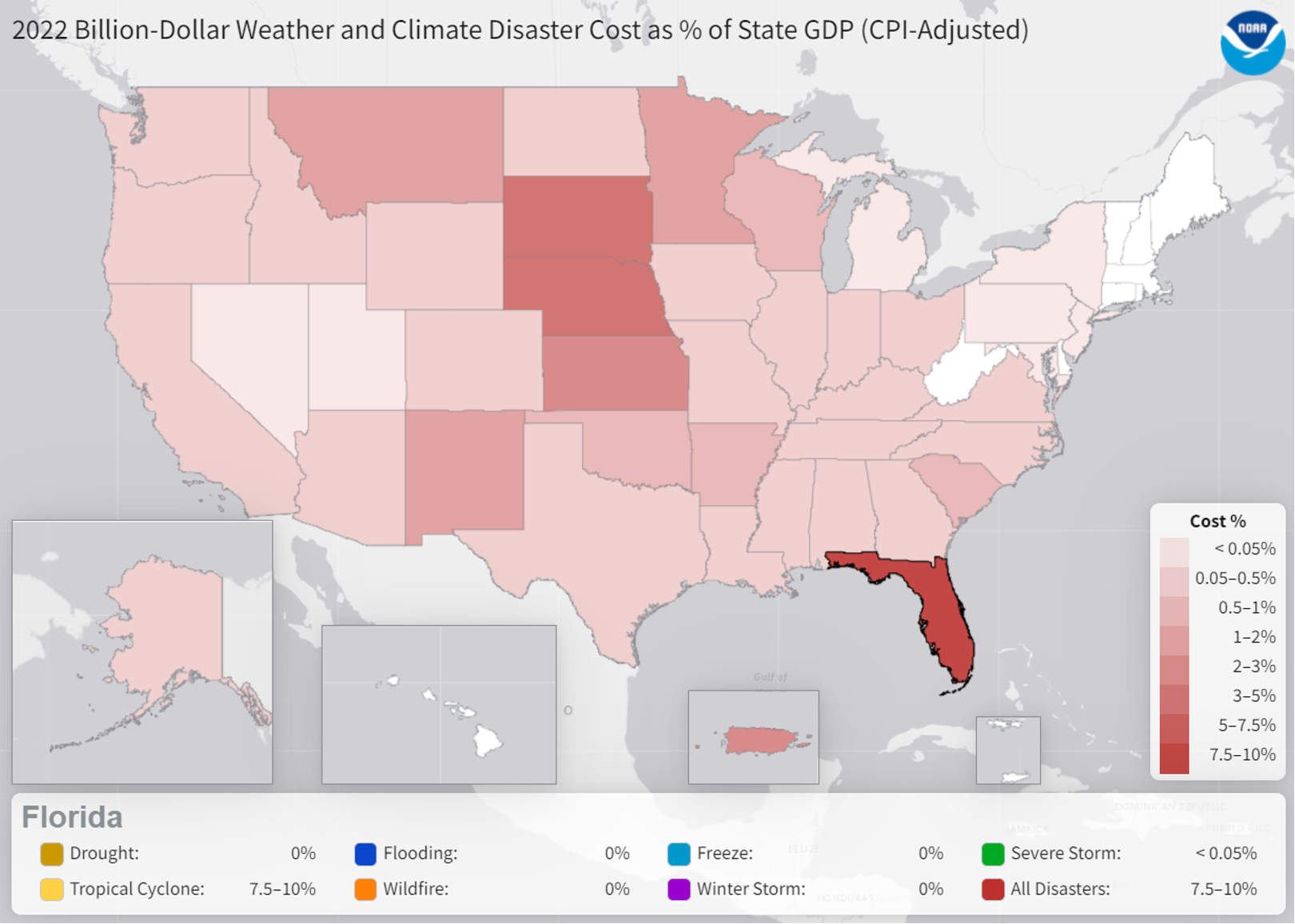

As a a born and raised Floridian, I'm not surprised to see that Florida is one of the leaders in climate disasters. However, I was surprised to see that the costs of these disasters accounts for 7.5% - 10% of Florida's GDP. It's no wonder that insurance companies are pulling out of the state at breakneck speeds. It also calls into question the viability of the state's economy as a whole. How much of state's GDP can go towards relief for natural disasters before the economy collapses? As much as it pains me to say, I'm not sure I could move back to my home state knowing the risks.

Check out your county's risk profile here: Billion Dollar Weather and Climate Disasters

Practical Steps to Protect Yourself and Your Family

As a Financial Commando you will want to take some practical steps to ensure you and your family are protected from natural disasters. The first step is to use time-tested wisdom in selecting a place to live. Take the time to research the unique risks of a disaster you might face.

Here are a few considerations to keep in mind:

- Choose a place with some elevation. High ground is just as advantageous when dealing with flooding as it is an armed combatant.

- Check out FEMA's National Flood Hazard Layer (NFHL) Viewer and enter your address to see what your risks are for flooding.

- Choose flat or gently sloping ground. People often overlook the risk of mudslides or rock slides when choosing a home. Elevation alone won't save you if a bolder comes tumbling down on your house.

- Avoid living on the coast of the Southeast United States if at all possible.

- Avoid living in places with known earthquake risks.

Financially, you ought to assess insurance options for flood insurance and earthquake insurance if you are exposed to those risks. Please keep in mind that mudflows are typically covered by flood insurance, but landslides are not typically covered by earthquake insurance. For landslide or sinkhole coverage you should look to earth movement insurance which covers a broader set of perils than earthquake insurance. Make sure you have an in-depth conversation with your insurance broker to understand what perils your policy protects you from and the costs associated with it.

There is an option available for people who are exposed to several risks not normally covered by homeowners insurance. This insurance option is called a Difference in Conditions (DIC) policy. Typically this type of insurance is leveraged by larger organizations but individuals can ask their insurance brokers for these policies as well.

Insurance policies to consider:

- Flood Insurance

- Earth Movement Insurance

- Earthquake Insurance

- DIC Insurance

With all of that said, you may find that the extra insurance costs are too expensive for your budget or that there simply are not insurance companies willing to offer, or in some cases forced to offer, these insurance policies. If you find that is the case, then you may need to make a tough decision to live with the risk of losing your home, taking the steps to move to a lower risk area or finding ways to otherwise protect your property physically (sandbags?). None of these options are particularly appealing but neither is losing your home to a flood or mudslide.

As Warren Buffett is fond of saying, "You don't find out who has been swimming naked until the tide goes out." Don't get caught without a bathing suit.

Disclaimer: This blog post is intended for educational purposes only, it should not be construed as tax advice or financial planning advice. Consult a professional for tax and financial planning advice before making any changes. All photos are from open source domains.