Incremental Escalation is the strategy whereby a nation increases force in a slow but steady manner to achieve some material objective.

Incremental Escalation has been used as a strategy for aggressive nation states such as Russia, Iran and North Korea for many years. Some might argue that China has been using this strategy for the last decade or two as well. We are now seeing the same strategy being employed by Western states in support of Ukraine as more resources and higher quality resources are committed to supporting Ukraine with each iteration of aid.

Nation states are not the only ones that can benefit from this strategy, we can too!

Incremental escalation is effective because its approach calls for a light touch, making it more palatable for the one who adopts the strategy and less inflammatory for those who might oppose them.

In our financial lives we can use this strategy to incrementally save more money each time we experience a pay increase. By making incremental changes we can make marginal advances without extending ourselves too far too fast. An example follows to help illustrate why this is such an effective strategy.

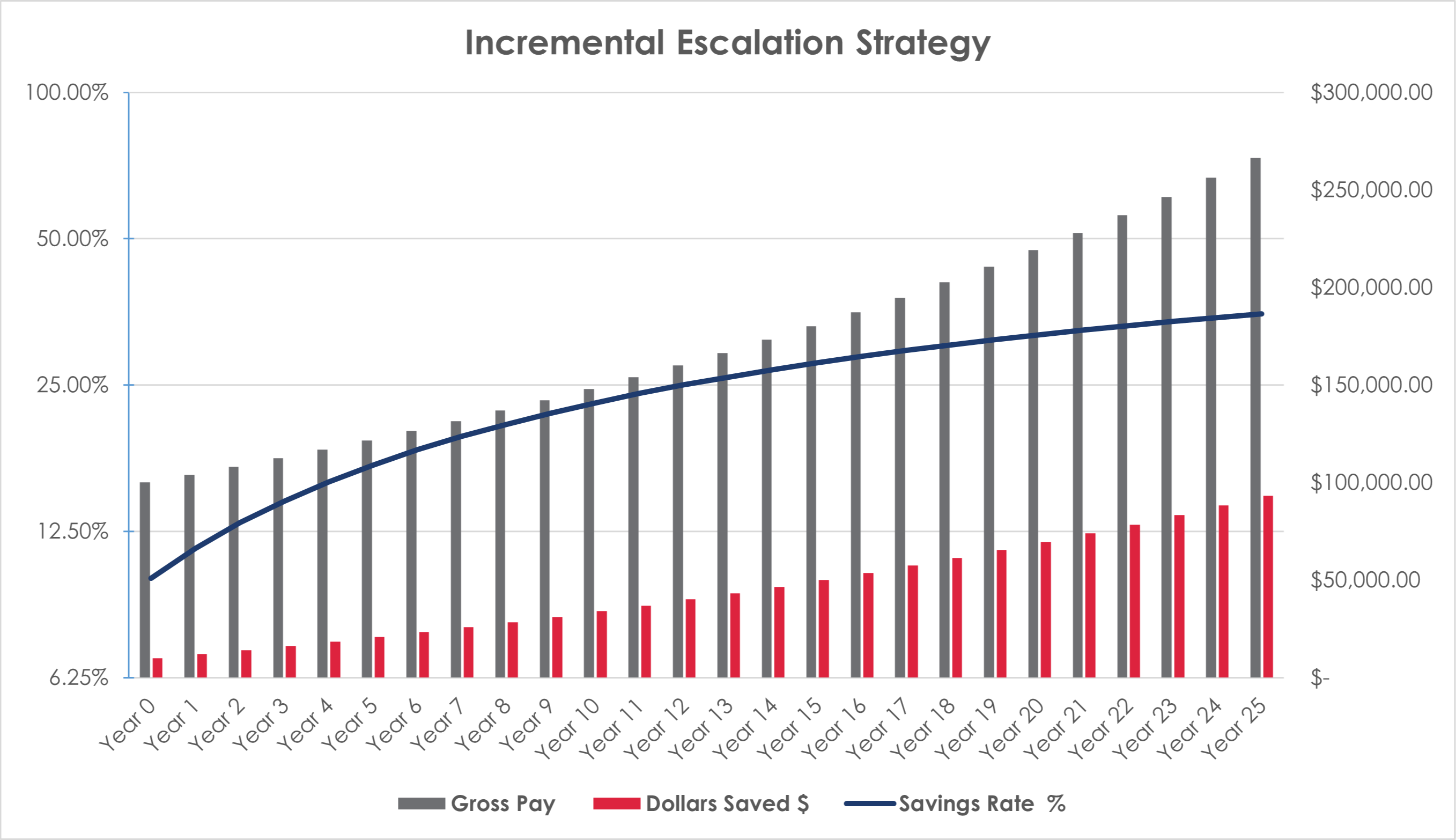

Let's assume our friend “Incremental Emanuel” wants to achieve a savings rate of 35% of his gross pay but he is currently saving 10% of his $100,000 salary. We will also assume he enjoys a 4% pay raise each year. For each pay raise he obtains he will commit to increasing his savings by 50% of the dollar value of his pay raises.

As the diagram illustrates, Emanuel who followed an incremental escalation strategy would enjoy more savings each year and an increase in gross pay less savings every year too. That is one reason this method is particularly attractive; it allows for some increase in expenditures while making progress towards financial goals. Assuming employment is constant, there is no reduction in spending on other priorities. However, Emanuel does get to enjoy an increase in spending and make progress towards his savings goals simultaneously.

How big of a difference does this make?

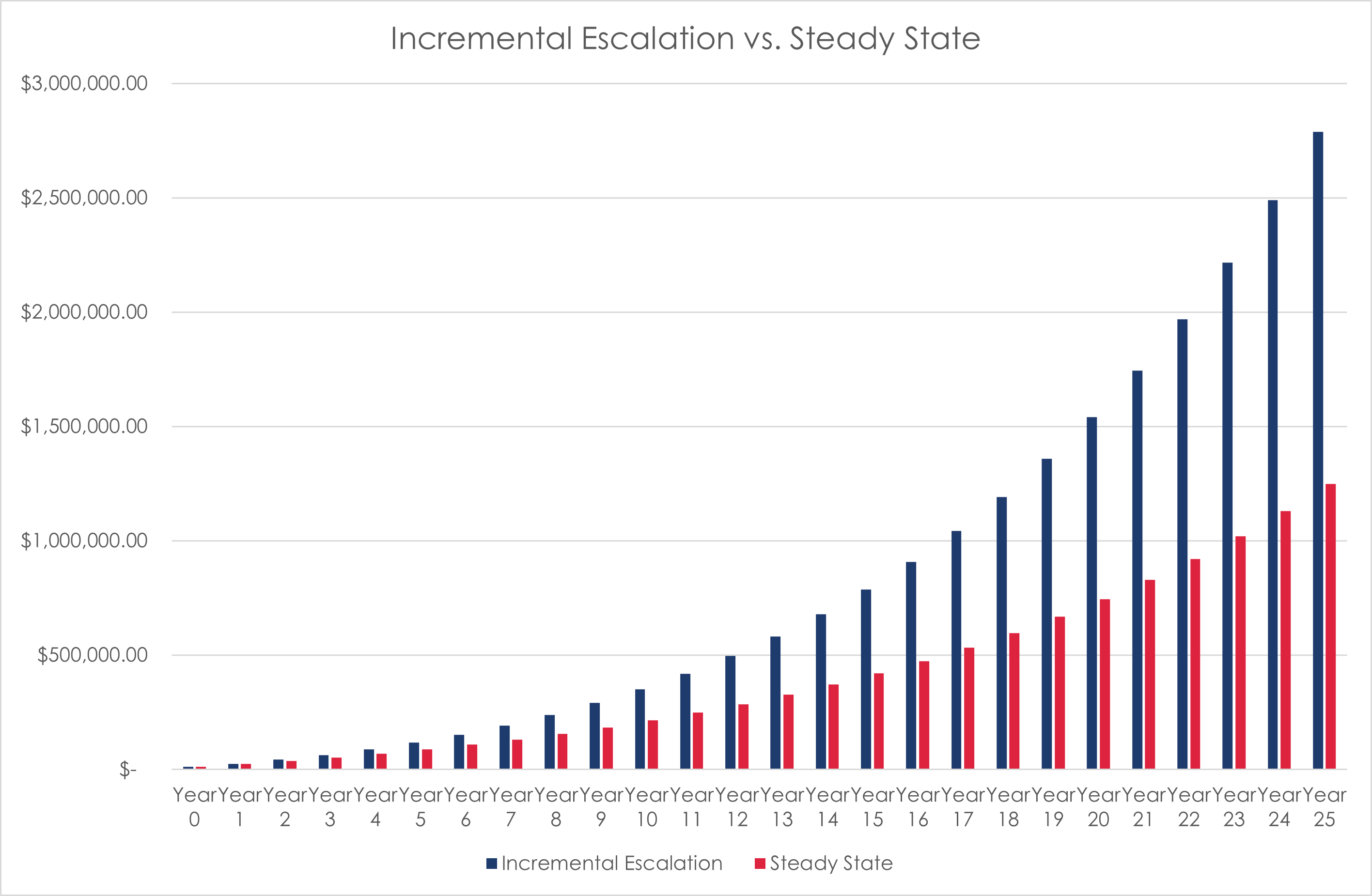

From our previous example, after 25 years of saving and investing with an 8% rate of return per year using the Incremental Escalation Strategy, Emanuel ends the period with more than double the amount of money as his buddy “Steady Eddie” would have who kept saving 10% of his gross salary despite Emanuel’s example. Since Emanuel chose the incremental escalation strategy, he ends the 25-year period with $2,788,212 compared to Eddie’s $1,248,449 who keep saving at a 10% savings rate. That is a difference of more than $1.5 Million.

The difference in what this means for maintaining quality of life is not 100% clear at this point yet. Let’s take this exercise one step further.

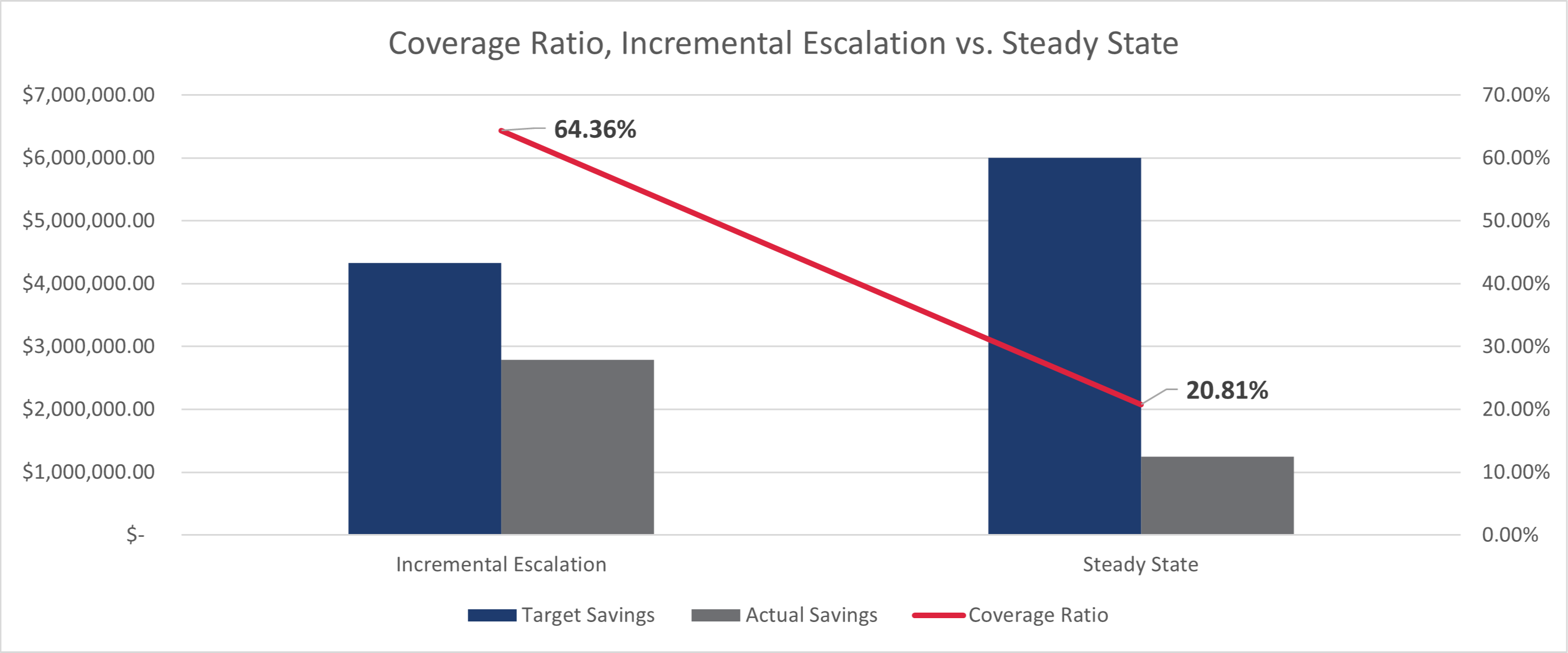

Inherent in Emanuel's decision to increase his savings rate he is also choosing to limit his lifestyle creep. Lifestyle creep is the phenomenon whereby our expenses expand to match a person’s take home pay. Emanuel, who chose the Incremental Expansion Strategy, ends the 25-year period with gross pay less savings (let’s call this annual expenditures) of $173,292 per year. However, Steady Eddie who chose to maintain his savings rate of 10% would have let lifestyle creep balloon his annual expenditures to $239,925.

It seems that Incremental Escalation can work against us just as easily as it can work for us.

Using a multiple of 25 times to estimate the amount of money required to maintain annual expenses for Emanuel and Eddie, we find that Emanuel has a target of accumulating $4,332,295 compared to Eddie’s target of $5,998,132. That means that after 25 years of saving and investing Emanuel would have saved 64.36% of his target and the Eddie would have only saved 20.81% of his target.

Disclaimer: This blog post is intended for educational purposes only, it should not be construed as tax advice or financial planning advice. Consult a professional for tax and financial planning advice before making any changes. All photos are from open source domains.