Perhaps the single most foundational exercise in wealth building for any member of the military or veteran is creating a budget and sticking to it.

Why? Because maintaining positive cash flow over a long period of time is the lifeblood of any effort to build wealth. We also never get access to the equity in the organizations we work for as members of the military or in civil service positions that our non-military peers may get access to through their civilian jobs. We don't get access to the same pay through equity as others do while we are serving and so those big paydays are off the table for us.

I know a lot of people cringe when they hear the word budget because to them it represents a chore that reminds them of misdeeds and regrettable decisions. However, when approached with the proper mindset, budgets are a thing of beauty because they reveal ways in which you can generate more wealth for you and your family, but it only works if you maintain the discipline to stick to a budget.

The reality is that no matter how wealthy you get, you are always only one bad decision away from blowing up your financial life.

Shortly after my first deployment, to Iraq, I created my first budget. It was the cornerstone of my wealth building journey that ultimately led to me reaching financial independence in my mid-thirties.

In my experience as a financial advisor, I have witnessed a strong relationship between keeping a budget and wealth creation with my own clients. My observation is not out of the norm. Dave Ramsey has famously noted that research his company performed found that as many as 93% of millionaires keep a budget. Achieving any significant and durable level of affluence or wealth is usually not an accident but done so with intention and discipline.

The bottom line is that treating your finances with intentionality by implementing a budget often results in better financial outcomes.

What is a Budget?

A budget is typically defined as an estimate of what you believe your income and expenses will be in a future period of time. While that is a decent enough description for the average person, who will likely go through their entire life without making a budget, we can improve upon it.

A budget, for the purposes here of building wealth, is better described as:an intentional plan to allocate each dollar of income during a given period of time to match your saving and expense targets by category such that every dollar is accounted for and allocated in a way that reflects your financial goals and aspirations.

What I am describing here when I refer to a budget is an alignment of your financial life with your personal values, goals and aspirations. It is a premeditated process that is done with intention by setting specific goals and targets in a time bound manner.

What is Not a Budget?

Many people will mistake tracking their income & expenses with creating a budget. Tracking expenses is a necessary part of keeping a budget but it is not in itself a budget. It differs in two fundamental ways. First, tracking your income and expenses happens after the fact. Second, tracking your income and expenses is an act of observation not an act of planning with intention.

Budgeting happens before a period of time occurs and sets targets for savings and expenses. Tracking income and expenses observes what occurred after the fact without regard for targets or a requirement to have targets at all.

As any good financial commando knows, targets get hit.

If you fail to set targets in your financial life, don't expect to hit any.

How to Implement an Effective Budget

Implementing a budget that actually works for you requires the development of a system. Here is the system I use and believe is effective for most people when creating their first budget.

- Create or find a zero-based budget template that has categories for income, savings and expenses.

- Ensure that expenses are divided into the following categories: regular expenses, variable expenses, and irregular expenses.

- Without looking at your income, savings and expense history, fill out the template by allocating each dollar of income to income, savings and expenses such that there are zero dollars from income that have not been allocated to either savings or expenses.

- Set your targets in the following order so that you get in the habit of paying yourself first:

- Retirement Accounts

- Other Savings Accounts

- Fixed Expenses

- Variable Expenses

- Irregular Expenses

- Track your income and expenses once per week to identify categories in which you are under or over spending.

- Make necessary adjustments to your budget to reflect real world trade-offs you must make so that you can achieve your desired savings rate.

Creating a Financial System that Works for You

One of the hardest parts about budgeting is that money is fungible. That is to say that any dollar saved, for whatever purpose, can be replaced by any other dollar that might have been saved for another reason. Often times when I encounter someone who is in dire financial straits, this is the root of the problem. You may recognize this phenomenon by another name, Robbing Peter to Pay Paul, or as mental accounting.

Since money is fungible, or interchangeable, people have a tendency to save money for one purpose only to spend it on something completely different. How many times have you heard a story about someone saving money to buy their next car only to use it on a fancy vacation instead? I hear about scenarios like these all the time.

What can we do to guard against this tendency?

The answer lies in creating friction and turning mental accounting into real accounting.

My solution to this problem is to create and maintain different accounts for different budget categories.

A common example of this is one that occurs by necessity, namely your retirement account. For legal and tax purposes, the federal government requires retirement accounts to be separate from your other funds so that they are more easily tracked and taxed appropriately. Theoretically, this could be done without setting up separate accounts. We could have a system in which we simply reported to the government how much of our funds we put into any normal saving or investment account was meant for retirement and what portion was not. Then the government could tax us accordingly. If this hypothetical system seems like a system that would obviously not work, then congratulations! You intuitively understand why most people's budgets don't work.

By segregating our money into different accounts, and even sometimes different financial institutions, we help our brains more easily conceptualize which pots of money are for what purposes. We are then less likely to violate our own budgets because we have created friction by forcing us to go into a system and transfer money from one account to another knowing full well that we are not acting in alignment with our stated goals and values.

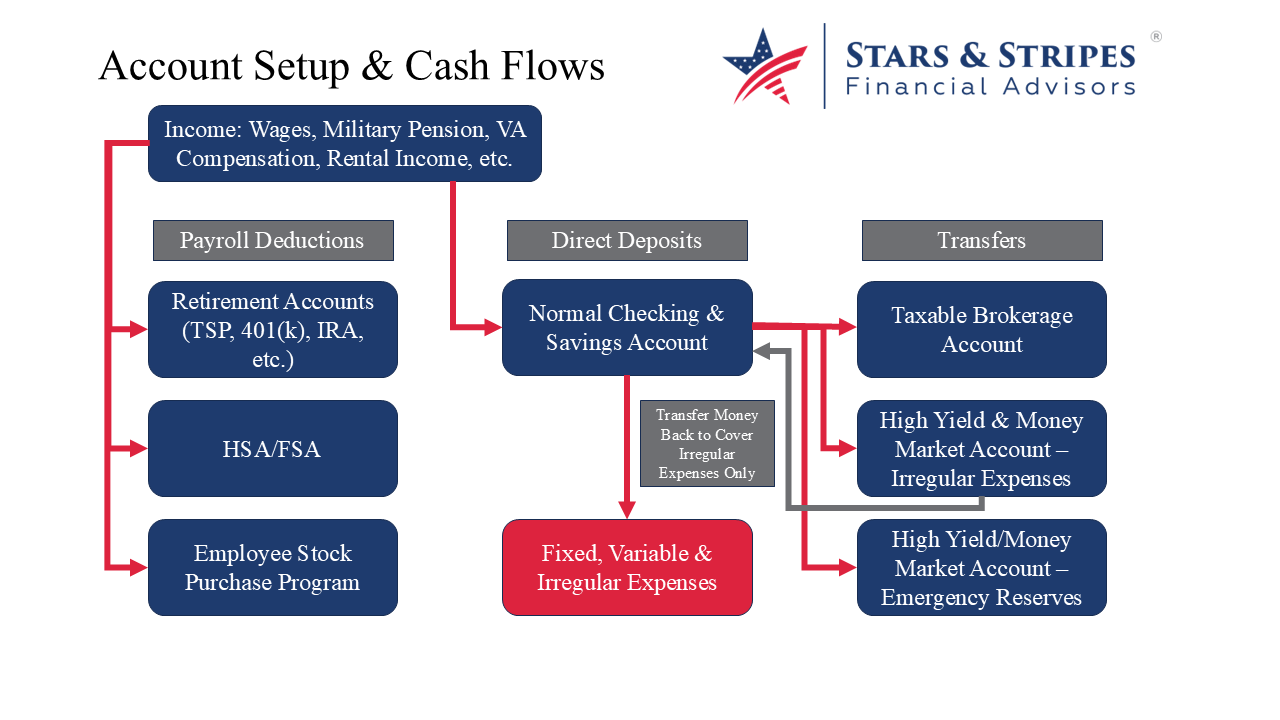

One common way to set up this system of accounts looks like the following:

- Retirement Accounts (TSP, 401(k), IRA, etc.): Contributions each pay period for retirement savings and investments

- Linked Checking/Savings Accounts: Direct deposit of funds from wages, military pensions, VA Compensation, Rental Income, etc. Accounts have auto draft functionality. Maintains 1.5 - 3 months of expenses in cash.

- High Yield Savings/Money Market Account: Receives transfers every pay period from normal checking/savings account. Account holds funds for emergency reserves/irregular expenses. Maintains 3 - 9 months of expenses in excess of regular checking/savings account. May be separated further into two accounts, one for emergency reserves and one for irregular known expenses. Commonly this account is at a different financial institution than your normal checking or savings accounts but not always. There is no auto draft functionality between this account and your other bank accounts.

- HSA/FSA Accounts: Contributions each pay period deducted directly from your paycheck. Funds and accounts are segregated for tax purposes. Money used for qualifying purposes only.

- Taxable Brokerage Accounts: Contributions made from normal checking/savings accounts every pay period. Money is saved and invested for long-term wealth building and other financial goals.

A diagram of the above example might look like the following.

As the diagram illustrates, it is reasonable to expect that a person may easily have six or seven different accounts. For married couples you may even require more accounts so that you can segregate funds based on expenses you want to keep separate from the relationship's joint expenses.

It is through this segregation of funds by distributing money into separate accounts that we can better organize and keep track of what money we have saved for specific categories. It makes it much easier for us to understand and allows us to hold ourselves accountable against our budgets. Budgets aren't important in and of themselves. Budgets are only important to the extent that they help us realize our own financial goals and objectives.

If you have questions about how make a budget or have other questions, schedule a consultation today or contact us to get your questions answered.

Disclaimer: This blog post is intended for educational purposes only; it should not be construed as tax advice or financial planning advice. Consult a professional for tax and financial planning advice before making any changes. All photos are from open-source domains or are the property of Stars & Stripes Financial Advisors.