Every skillset involves fundamentals. Often what separates a novice from a world class expert is a fluency of understanding and experience with the fundamentals of their craft. In the military we learned about the fundamentals of marksmanship, troop movements, etc. and over time, with study and practice, we became experts in our domains. Our financial lives are no different.

This blog post will focus on a few fundamentals of personal finance that any high-speed low-drag financial commando needs to know.

The Big Four

In the world of finance there are four big accounting terms that everyone should understand if they want to be proficient with money. Namely they are Income, Expenses, Assets and Liabilities. Income and expenses belong on your income statement, and assets and liabilities belong on your balance sheet. Whenever you think about anything in the realm of finance it is best to think of it relative to something else that compliments it. Naturally that is why we want to see our income relative to our expenses and our assets relative to our liabilities. But more on that later.

You are probably somewhat familiar with The Big Four. However, I'd like to discuss not just what they are, but how they interact with each other and how to exploit them to get ahead in your financial life. To that end, let's get started with the income statement.

Income Statement

The income statement is a critically important financial statement. It shows not just how much money is coming in but how much is going out. By having both of these figures together we get a better idea of not just what we are making but how much it we are keeping. And, after-all, it's not how much we make that matters but how much we keep. On the income statement we call this difference between what we make and what we spend cash flow. Cash flow can be either positive or negative. The accounting equation looks something like this: Income - Expenses = Cash Flow.

Income

Usually when I bring up income the first thing that pops into a person's mind is actually something called wages. Wages are what you earn from your job, but income is defined as any form of money you receive from working or investments. A few examples include: wages, royalties, capital gains, interest and dividends. The word "income" comes from Middle English and is the combination of "in" + "come". So, when you say income you are literally talking about money "coming in".

Expenses

If income is any money that is coming in then expenses are any money that is going out. The word expenses comes from the Latin word expendere which is derived from the combination of "ex" + "pendere". Ex in Latin translates to out, and pendere translates to pay. In other words, the word expenses was derived from another word which literally means "pay out". You'll notice that income and expense are exact opposites of each other but that they also perfectly compliment the other. That is to say that as long as money is coming or going, in any form, then they should be captured under the umbrella of either income or expense.

On the balance, it doesn't much matter what your income or expense levels are at the end of the day. Rather, what really matters is how much your income is relative to your expenses or vice-versa. You financial commandos out there will recognize that any income in excess of your expenditures is something called positive cash flow or net income. Unfortunately, it is possible for you to have more money going out than coming in and when that happens we call it negative cash flow.

When you have positive cash flow, or money left over after all of your expenses, then you can save that money and increase your wealth, which is a great segue into the next section about the Balance Sheet.

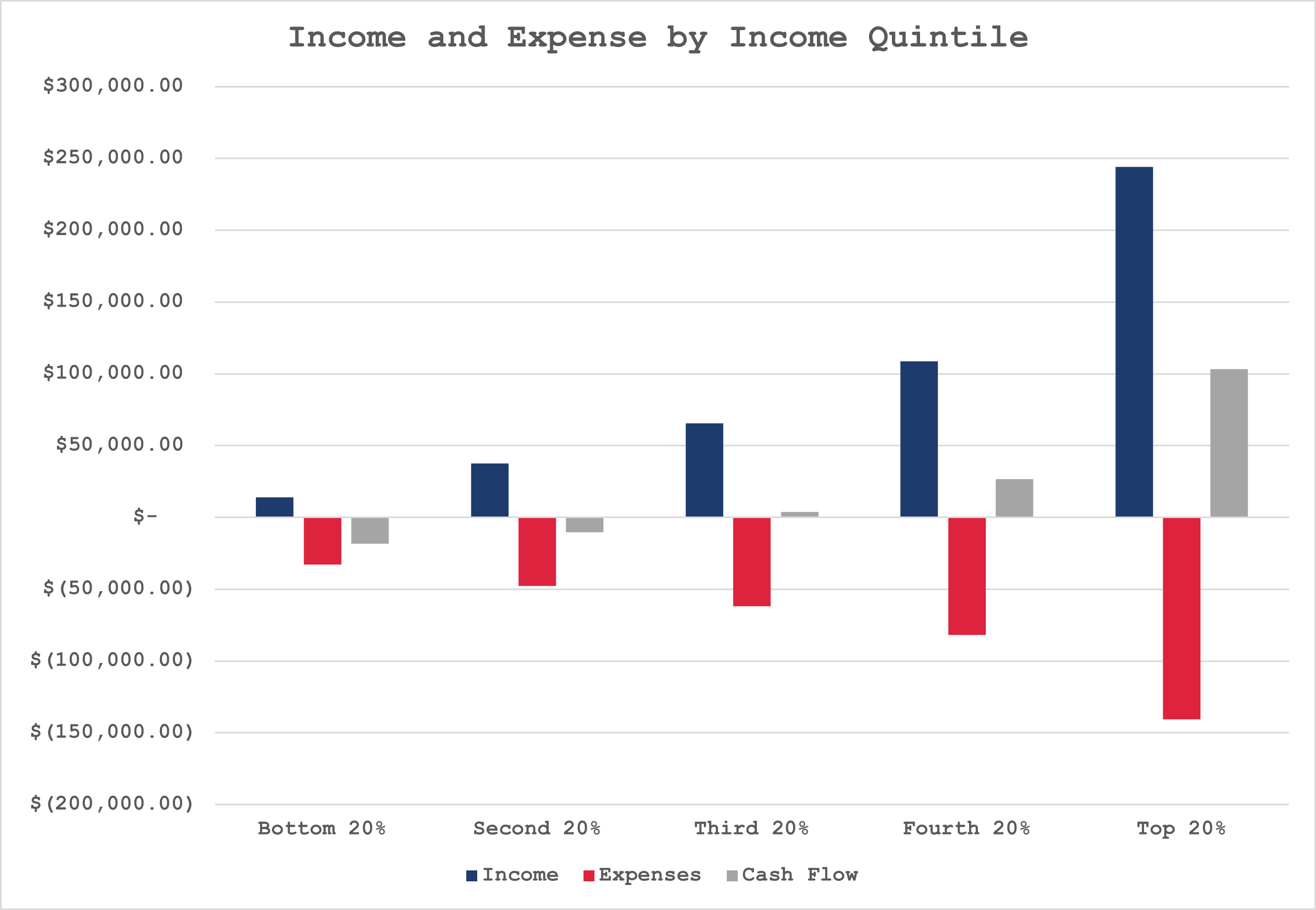

Below is a picture of the income, expenses and cash flow of the average house in the United States by income quintile for 2022. As you can see, your cash flow depends on both your income and expenses.

Balance Sheet

If I had to choose a favorite financial statement I would choose the balance sheet. It gives you a snapshot of your overall financial well being at a moment in time. This is particularly important because it gives you a score card for tracking your wealth. While the income statement can show you how much money you made and kept during one period, the balance sheet can reflect the result of your savings and investments over the course of your entire life.

The balance sheet is named such because it is meant to balance. In the world of accounting the equation for a balance sheet looks like this: Assets = Liabilities + Equity. Equity is also known as net worth when it comes to your personal finances. You can think of it as what the grand total of your wealth would be if you paid off all of your debts. It is that one metric which is the yard stick by which we measure someone's overall financial wellbeing.

Assets

Assets are defined as anything that is useful or valuable. The Latin word Adsatis is the predecessor of asset. If you split the word apart into its component parts you will find that "ad" + "satis" means "to" and "enough". In short, assets mean to have enough. Enough for what? I suppose it depends, but the idea is that you have something and that's more than a lot of people can say.

Sometimes this presents a problem for people when they are trying to understand how well off or not they are. That is because there are two types of assets generally speaking. There are personal use assets such as a car, couch, tv, etc. and there are financial assets such as stocks or bonds. While we typically assign a value to each we also recognize that personal use assets generally decrease in value over time and cost us money in the long run. On the other hand, financial assets generally provide us with some form of income or appreciation in value over the long run. Or at least we hope so!

You can imagine that your financial well-being might be very different if you had $100,000 of furniture versus $100,000 worth of stock in strong companies. That is why it is best practice to ignore most personal use assets unless they will likely be sold or exchanged for a significant amount of value in the future.

Liabilities

The definition of liabilities is "a thing for which someone is responsible". The Latin word ligare means "to bind or tie up". So when we think about the word liabilities we should think of being bound by some responsibility or even becoming a financial POW. In the military we sometimes referred to someone who wasn't trained well enough as a liability because they could really bind you up in a pinch, and nobody wants that. Just the same, a financial liability is also a burden that is felt most prominently when things get tough.

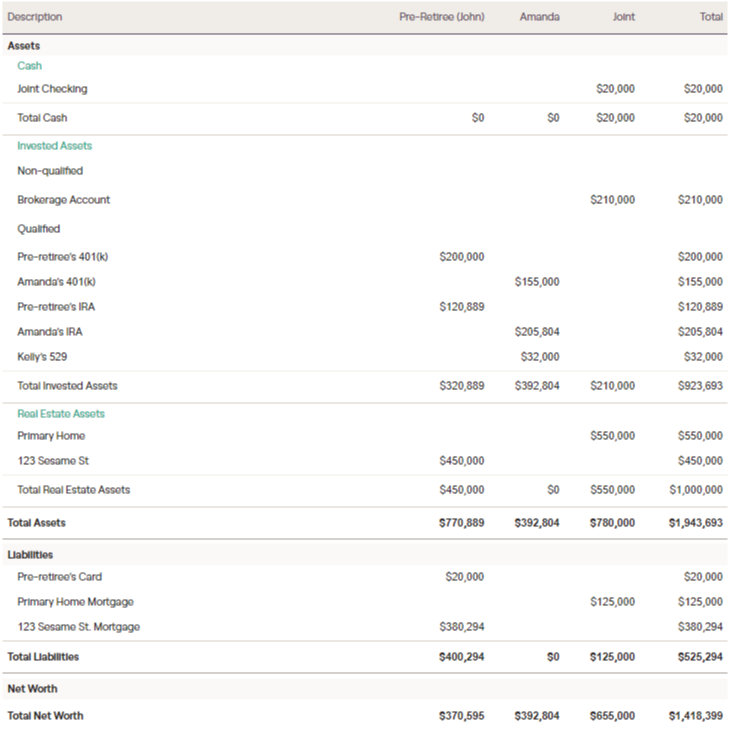

If you want to get a look at what your income statement and balance sheet might look like then feel free to try out my financial planning software.

Disclaimer: This blog post is intended for educational purposes only, it should not be construed as tax advice or financial planning advice. Consult a professional for tax and financial planning advice before making any changes. All photos are from open source domains.