Financial Independence Retire Early, otherwise known as "FIRE", has seen a growing following in the last few years as a new generation enters the work force. As a member of the community myself, I often get asked about this topic and so I wanted to write a blog post about to help my readers understand what it is, how to accomplish it, and why it may not be as glamorous as you think.

What is Financial Independence Retire Early (FIRE)?

First, let's break it down into its component parts. Financial Independence at a basic level is having enough passive income or assets to cover your expenses for the remainder of your life without having to work. Another way of describing this is to say that someone has retired. Afterall, what is retirement if not being in that phase of life in which you no longer have to work? That is where the "Retire Early" part comes in. It is an acknowledgement that by becoming financially independent before Normal Retirement Age (NRA) you have achieved something unique by retiring early.

While you can theoretically become financially independent at any age, you may choose to forego the early retirement part. Many people in the community would still say that you have "FIRE'd" because really the movement is more about the independence than it is sipping daiquiris on the beach. As a result, I usually just refer to it as being financially independent and leave the retire early part.

To put a finer point on it, it is important to recognize that financial independence is different from something like homesteading. Homesteading is about true self-sufficiency in a natural state. Financial independence for most people has little to do with how you live your life relative to technology or society, and is more strictly about the financial independence from your job. There is a myriad of ways to become independent from society, a job, family, etc. without necessarily becoming independent from work. For example, we wouldn't say that a reclusive author is financially independent if they still need income from new books yet to be authored even if they do in-fact only work for themselves at this point.

While this may be taboo to say in the FIRE community, really the concept of financial independence is really just the early stages of affluence (AKA wealth).

Achieving Financial Independence as a Veteran

Financial Independence for veterans, and non-veterans alike, boils down to a mathematical formula. Effectively, this mathematical formula seeks to have your projected life time income exceed your projected life time expenses with a confidence level of 95% or greater. Where things get tricky is in calculating future income and expenses because we don't actually know what inflation will be or what investment returns will be in the future. This requires projections to be done to determine how likely it is a person has achieved financial independence and a careful review should be done of insurance needs as well. I'd highly recommend getting your information looked at by a professional before making in drastic life changes on account of feeling that you have achieved financial independence.

How to Achieve Financial Independence

The wealth building process for those people who achieve it through their own work follows a simple mathematical formula that anyone with a finance degree will recognize immediately.

A = P(1+r/n) ^ (nt)

Where:

- A = Assets

- P = Principal invested

- r = Rate of return

- n = Number of compounding periods per year

- t = Number of years

In this formula you want the A to represent the amount of assets you need to produce the passive income that will offset your expenses that are not covered by pensions or other guaranteed income.

That leaves us with a few levers that can be pulled to accelerate the accumulation of wealth in an effort to achieve financial independence. We have the amount of money that is invested every year (how much money is saved), the rate of return we make on the money that is saved, and the number of years the money continues to be invested and earn compound interest.

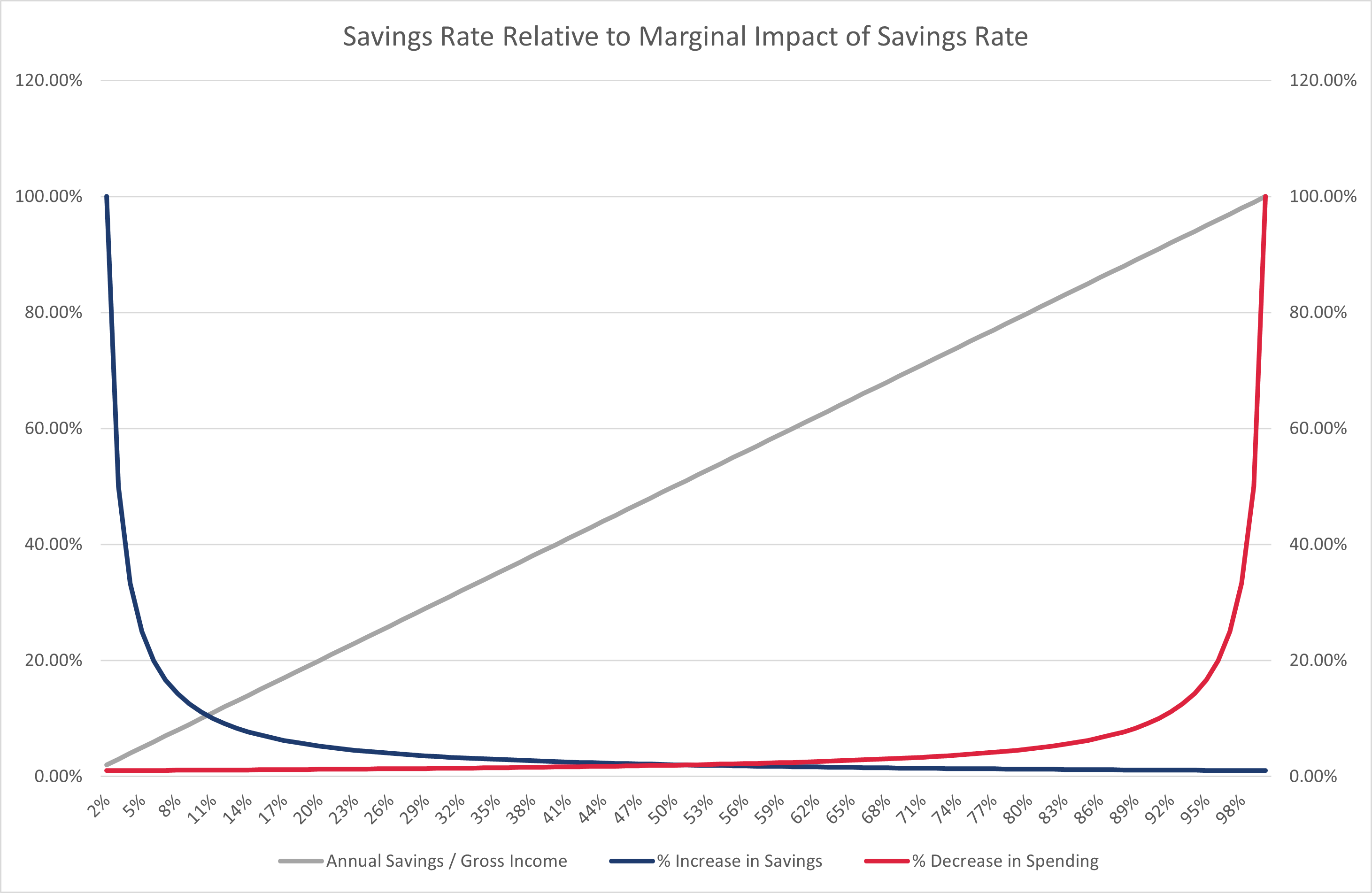

As we begin to save, we go from a savings rate of 0% to 1%. This represent an infinite increase in our savings rate and is hard to graph. However, from a savings rate of 1% to 2% we see a marginal increase of 100%. From 2% to 3% we see a marginal increase of to our savings rate of 50%. At the same time our purchasing power, or the percent of our gross income devoted to spending goes from 100% to 99% which is only a 1%-point decrease in our spending. When we go from a spending rate of 99% to 98% this is only a marginal decrease in our spending rate of 1.01%. The following graph demonstrates this relationship.

From this graph I want to make a few key observations.

- Increasing your savings rate from 10% to 11% results in a marginal increase in your savings rate of 10%. That is the first point at which the marginal impact of additional savings is less than the total savings rate. That is illustrated in the graph as the inflection point where the grey line and blue line intersect.

- The second inflection point occurs at the 50% savings rate where the red line and blue line intersect. At this point, each additional dollar saved results in your marginal expenses going up by a faster rate than your marginal savings rate.

What this graph and relationship suggest is that is that increasing your savings rate between 0% and 10% has asymmetrical benefits relative to the costs. It also demonstrates that the marginal impact of increasing your savings rate from 11% to 50% is beneficial on the margin relative to the cost you bear even if the marginal benefit deteriorates along the way.

One formula for estimating the dollar value of the assets you might need in perpetuity is the following:

A = E x 1/(re - ie)

Where:

- A = Assets

- E = Annual expenses

- re = Estimated rate of return

- ie = Estimated inflation

Let's take a look at a simplified example to illustrate how some of the math works. Our example will assume annual expenses of $60,000, estimated returns of 6% on average and estimated inflation of 3%. We adjust for the rate of inflation to maintain purchasing power and the principal invested. The importance of maintaining the principal is to maintain financial independence for an unknown period of time that will likely stretch for decades. We will also ignore tax implications and return variations for simplicity’s sake. Therefore, you would have the following:

- A = $60,000 x 1/(.06 - .03)

- A = $60,000 x 1/.03

- A = $2,000,000

But we must also keep in mind that the level of assets needed is directly proportional to the level of expenses which need to cover. In other words, as our savings rate increases our expenses necessarily decrease and as a result our required assets for financial independence decreases in-kind.

For example, if I choose to save at a rate of 10% then I could only possibly require $54,000 of the original $60,000 of expenses to be covered. However, if I choose to save at a rate of 20% then I would only need $48,000 of expenses covered.

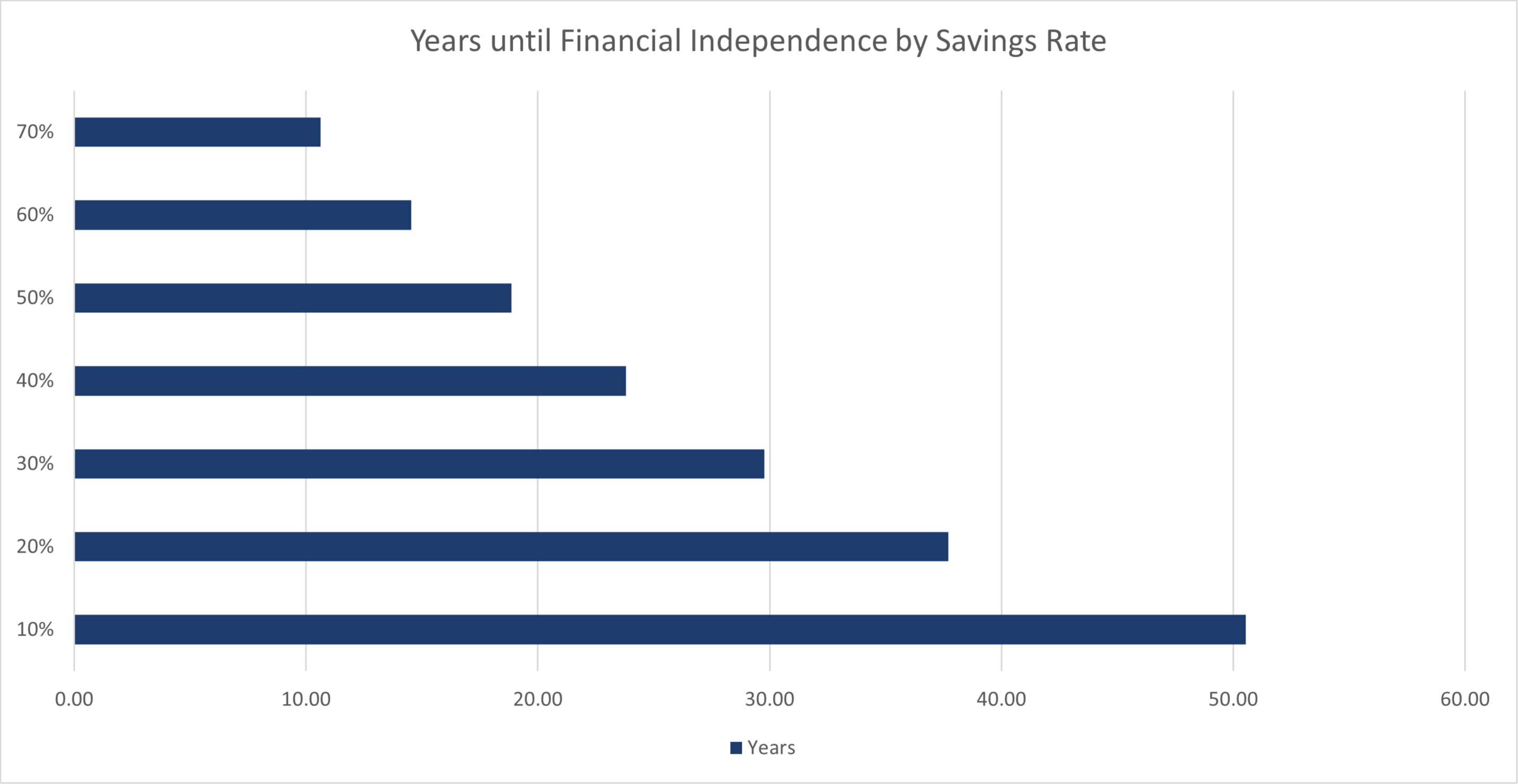

The following graph will look at how long it would take to save that much money given different savings rates assuming a rate of return of 6% and inflation adjustment of 3%.

While this is a simplistic model, hopefully it will provide a framework to better understand the relationships between how your savings rate and investing can impact how quickly you reach financial independence.

How Can Veterans Achieve Financial Independence?

Veterans typically have access to a number of advantages in building wealth and passive income towards the goal of financial independence that many others do not have.

One advantage that I used personally was to super charging my savings while on deployment. While I didn't make much money in terms of my wages during my deployments, I was able to drastically increase my savings rate thanks to being able to put most of my bills and expenses on hold. While deployed to combat zones military members also get incredible tax breaks. The combination of these two factors allowed me to save over 80% of my income during deployment. Clearly those supporting families while deployed will not have the same luxury but there should still be an ability to increase savings to some extent.

Another incredible advantage that military members have working for them is the opportunity to earn a military pension. Military pensions have a few distinct characteristics that can provide an incredible amount financial benefit to someone seeking financial independence. The first is that the annuity from a pension is a cash flow that will last for the remainder of your life. If you are keeping track of the math, in our example above each dollar earned via a military pension is means you have to save $33.33 fewer. For example, if you earned $30,000 per year through your pension, that would mean you have to save $1 Million less given our example above. This same concept can be applied to for VA Disability Compensation as well. I have been ignoring taxes for simplicity’s sake in this post but a dollar of tax-free income from VA disability compensation is financially more advantageous than a dollar from a taxable military pension.

One advantage that veterans and military members have relative to their contemporaries who have not served is being conditioned to live in austere environments. Being comfortable with a certain level of discomfort allows a person to forgo some creature comforts which if directed accordingly can lead to a higher savings rate. With this discipline someone in the military can get a large head start on their wealth building journey.

Why Financial Independence May Not Be For Everyone

One common issue people run into with financial independence is a lack of purpose and a challenge to their identity. Anyone who has transitioned out of the military and into life as a veteran will already be familiar with what it is like to lose part of your identity as a member of community. Walking away from another profession and even the workforce entirely can be just as jarring when it comes to lack of purpose and identity. This can even happen to people who enter retirement at a normal age. Have you ever heard about someone becoming depressed after they retire?

The trick to keeping your head above water when you make this type of transition into retirement, early or not, is to stay engaged with people in your community and find a purpose while you are at it. The absence of purpose and social engagement is a one two punch that you don't want to be on the other end of.

My advice to anyone thinking about a major life transition like that is to think about a few things that might provide you with a sense of purpose and fulfillment then go do it with someone. There are no wrong answers as long as it brings you happiness and a sense of belonging.

Want to learn more about retiring from the military, or retiring in general? Click here to learn more.

If you have questions about how your military pension fits into your financial future, schedule a consultation today or contact us to get started.

Disclaimer: This blog post is intended for educational purposes only, it should not be construed as tax advice or financial planning advice. Consult a professional for tax and financial planning advice before making any changes. All photos are from open-source domains or are the property of Stars & Stripes Financial Advisors.